Dollar Cost Averaging

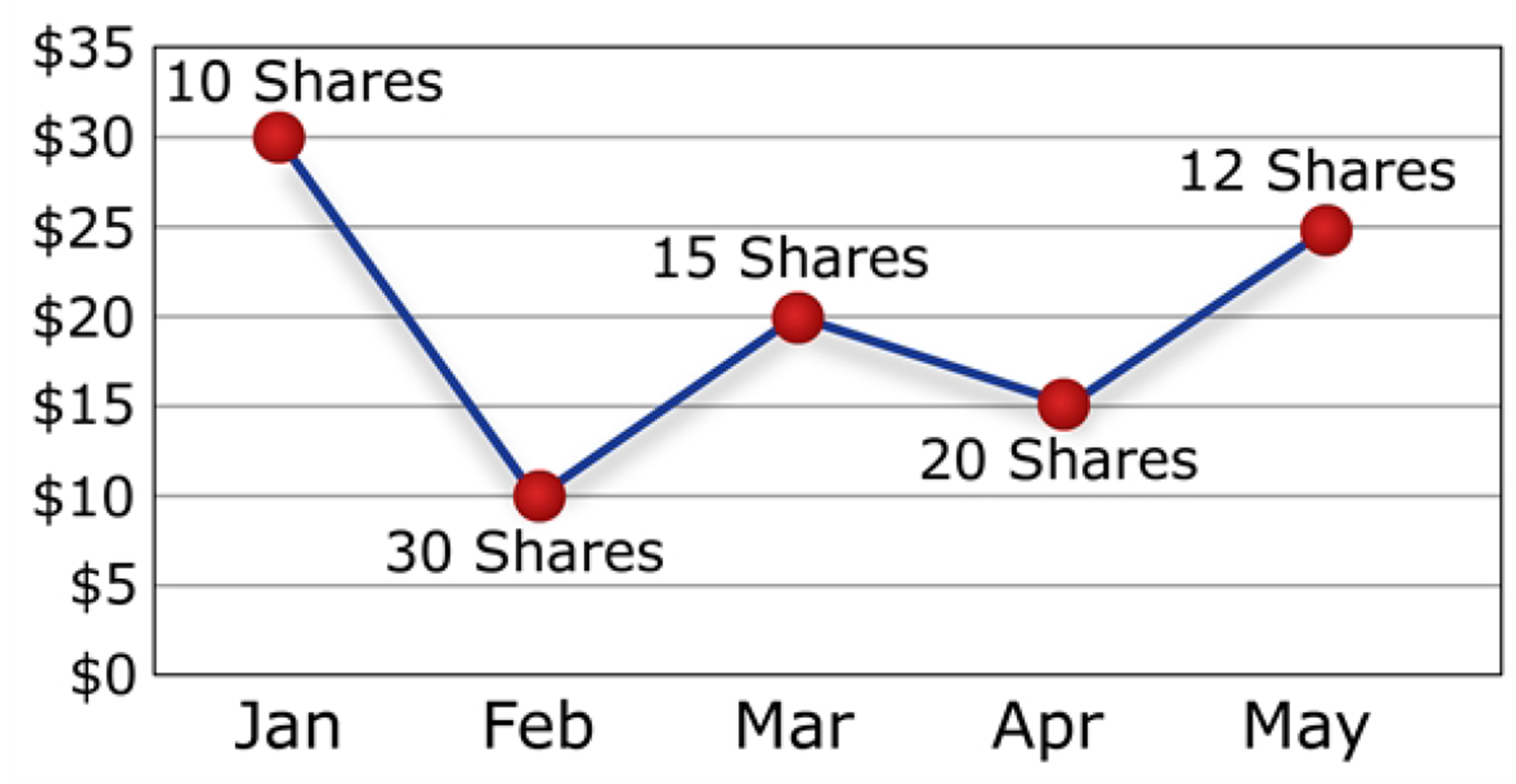

Dollar Cost Averaging is the process of investing equal amounts over a number of equally-spaced intervals into some form of equity that may vary in price over time. This has the effect of buying more units of the equity when prices are low, and fewer units when prices are higher.

In the case of Indexed Universal Life Insurance (IUL), dollar cost averaging also has the effect of spreading out the maturity dates of index buckets. Most insurance companies allow for lump sum payments to be gradually placed into the index strategy over the coming year - usually on a monthly basis - while retaining those as-yet unallocated funds to earn interest in its Fixed Account. For example, a person places $100,000 into the Fixed Account of an IUL policy as a lump sum contribution.  Regardless of whether or not he is also making other periodic premium payments, he might instruct the carrier to phase, say, $9,000 per month into new index strategy buckets until the Fixed Account is depleted. If, for example, that index strategy were the S&P, and the S&P fell over the first six months, followed by a rise in the second six months, the policy owner would be obtaining more units as prices fell, and fewer units as prices rose.

Since each bucket is protected from investment loss, having a zero floor, the policy owner stands to profit more from buckets that were created when the index was down, but not risk a loss when buying the index at its near-term peak price. It is also nice to have maturing buckets spaced evenly throughout the year, so as to absorb any charges made by the carrier on the policy, which are usually made on a monthly basis. (Back to IUL Table of Contents)

|